How to resolve AdBlock issue?

How to resolve AdBlock issue?

Business News

- Details

- Written by: Redwood Credit Union

SANTA ROSA, Calif. — Steve Greig has joined Redwood Credit Union, or RCU, as senior vice president of marketing and communications.

In his role, Greig leads the marketing and communications teams, driving strategic campaigns that amplify RCU’s products and services, while ensuring consistent messaging across corporate and member communications, public relations, marketing, and social media.

Greig is a seasoned marketing executive with over 30 years of experience in building brand value, driving growth, and developing high-performing teams.

Previously, as vice president of global marketing at Visa Inc., Steve led key global marketing initiatives across more than 200 countries, including Olympics and FIFA sponsorships and cross-border marketing.

He has also led marketing teams at fintech companies, including Fundbox and One Financial, and helped build some of the world’s best known beer brands, including Heineken, Newcastle Brown Ale, Foster’s, and Beck’s.

“I’m confident that Steve’s proven track record of strategic leadership will help continue to amplify our brand and reflect the purpose, values and service excellence that define RCU,” said Mishel Kaufman, RCU’s chief operating and risk officer. “We look forward to the innovation and insight he brings to this role.”

Greig holds a master’s degree in marketing from Strathclyde Business School in Glasgow, Scotland, and an MA Hons degree in history/European studies from the University of Dundee in Dundee, Scotland. He grew up in Edinburgh, Scotland, and now resides in San Rafael with his family. He enjoys fly fishing, music, films, and spending time outdoors.

Founded in 1950, Redwood Credit Union is a full-service, not-for-profit financial institution providing personal and business banking to consumers and businesses in the North Bay and San Francisco.

For more information, call 800-479-7928, visit redwoodcu.org, or follow RCU on Facebook, Instagram, X, and LinkedIn for news and updates.

- Details

- Written by: State Controller's Office

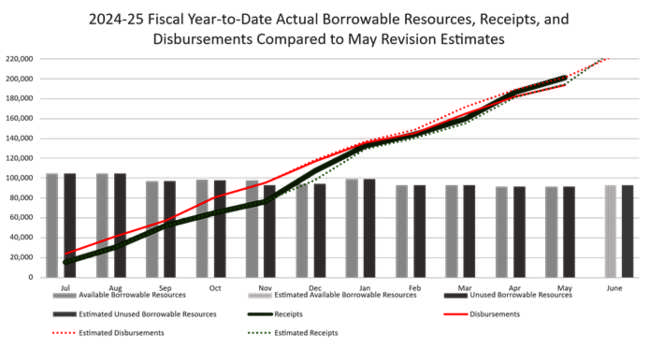

State Controller Malia M. Cohen this week released her monthly cash report covering the state’s General Fund revenues, disbursements and actual cash balance for the fiscal year through May 31.

As noted in the Controller’s Monthly Statement of General Fund Cash Receipts and Disbursements, receipts for the fiscal year through May were higher than estimates contained in the 2025-26 May Revision by $640.1 million, or 0.3 percent.

Fiscal year-to-date expenditures were $3.3 billion, or 1.7 percent, lower than Governor’s Budget estimates.

The state started the fiscal year with a $14.7 billion General Fund cash balance and ended May with a $21.7 billion balance.

“Even with rising economic uncertainty at home and abroad, the state’s strong cash position and its ability to pay its bills on time and in full continue with revenues and spending meeting expectations.” said Controller Cohen. “With the Legislature currently finalizing its spending plan for the fiscal year beginning on July 1, I encourage continued fiscal restraint coupled with maintaining reserves in the event the state faces increased volatility in its revenues or spending.”

For the fiscal year through May, personal income tax receipts were $374.4 million above May Revision projections, or 0.3 percent.

Corporation tax collections were $225.3 million, or 0.8 percent above estimates. Retail sales and use tax receipts were $255.3 million below recent projections, or 0.8 percent.

The Controller continues to note that while April 15 is the traditional annual personal income tax payment deadline, the Franchise Tax Board extended the current deadline for Los Angeles County individuals and businesses in response to the fires that began on January 7, 2025. These individuals and businesses have until October 15, 2025, to file and pay taxes.

As of May 31, the state had $91.5 billion in unused borrowable resources. These resources are from internal funds outside of the General Fund that are borrowable under state law and that the State Controller’s Office uses to manage daily and monthly cash deficits when revenue collections are lower than expenditures. Internal borrowing from special funds is short-term and is repaid so that borrowing does not affect the operations of the special funds.

The summary chart follows.

- Details

- Written by: Editor

LAKE COUNTY, Calif. — The Lake County Chamber of Commerce announced its Marquee Mixer of Summer 2025, a special joint event with the Calistoga Chamber of Commerce, on Wednesday, June 11, from 5:30 to 7:30 p.m. at the Greenview Bar & Grill in Hidden Valley Lake.

“This unprecedented collaboration marks a new era of cross-county connection and economic dialogue between Lake and Napa counties,” the Lake County Chamber said in its announcement.

This exclusive event will feature a presentation and Q&A with Kevin Case, offering a rare inside look at the Guenoc Valley Resort project — an ambitious development with the potential to reshape Lake County’s future.

Lake County residents and business leaders will have a unique opportunity to ask questions and hear directly about progress and vision for the project.

“This is more than a mixer — it’s a meeting of minds and momentum,” said Amanda Martin, CEO of the Lake County Chamber. “We are proud to partner with the Calistoga Chamber to foster regional collaboration and to provide our members with a front-row seat to what could be a transformative project for our economy.”

In addition to networking, the evening will celebrate Coleen Yorba Lee, who was recently honored with the International Certified Tourism Ambassador Award for 2025 — a prestigious recognition of her tireless dedication to promoting Lake County as a destination.

Guests will enjoy a wonderful array of appetizers and award-winning local wines from Fults Family Vineyards, Six Sigma, Wild Diamond, and Langtry for just $5 a glass. Admission is free for members of the Lake County, Calistoga, and Clear Lake Chambers of Commerce. Non-members are welcome for $25.

“Don’t miss this powerful evening of networking, insights, and celebration. Whether you’re a local business leader, community advocate, or curious resident, this is your chance to be part of Lake County’s next chapter,” the Lake County Chamber said.

- Details

- Written by: Small Business Administration

LAKE COUNTY, Calif. — The U.S. Small Business Administration, or SBA, is reminding small businesses and private nonprofit organizations in California of the July 7 deadline to apply for low interest federal disaster loans to offset economic losses caused by the Boyles Fire.

The fire took place Sept. 8 to 11, 2024.

The disaster declaration covers the California counties of Colusa, Glenn, Lake, Mendocino, Napa, Sonoma and Yolo.

Under this declaration, SBA’s Economic Injury Disaster Loan, or EIDL, program is available to small businesses, small agricultural cooperatives, nurseries, and PNPs impacted by financial losses directly related to the disaster.

The SBA is unable to provide disaster loans to agricultural producers, farmers or ranchers, except for small aquaculture enterprises.

EIDLs are available for working capital needs caused by the disaster and are available even if the small business did not suffer any physical damage.

The loans may be used to pay fixed debts, payroll, accounts payable, and other bills not paid due to the disaster.

“SBA loans help eligible small businesses and private nonprofits cover operating expenses after a disaster, which is crucial for their recovery,” said Chris Stallings, associate administrator of the Office of Disaster Recovery and Resilience at the SBA. “These loans not only help business owners get back on their feet but also play a key role in sustaining local economies in the aftermath of a disaster.”

The loan amount can be up to $2 million with interest rates as low as 4% for small businesses and 3.25% for PNPs with terms up to 30 years. Interest does not accrue, and payments are not due until 12 months from the date of the first loan disbursement. The SBA sets loan amounts and terms based on each applicant’s financial condition.

To apply online, visit sba.gov/disaster. Applicants may also call SBA’s Customer Service Center at 800-659-2955 or email

Submit completed loan applications to the SBA no later than July 7.